Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

Ferrous Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

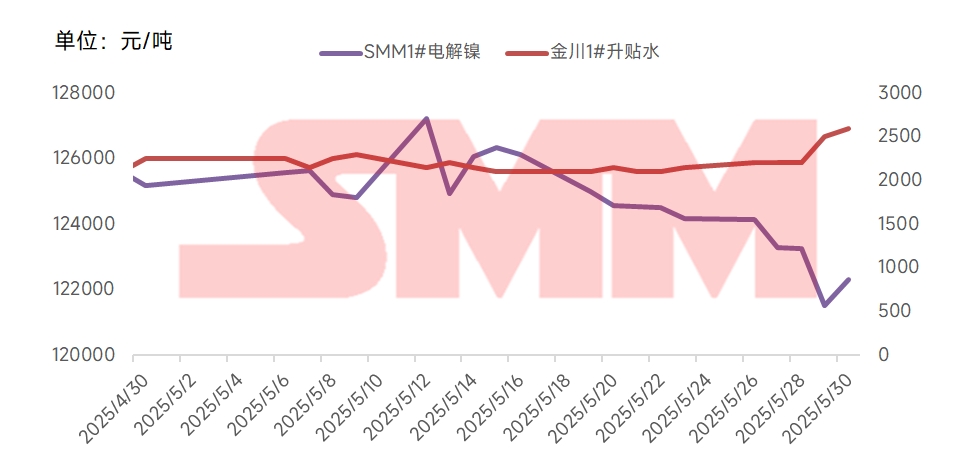

1. Spot Market: Weakening Premiums and Sluggish Trading Activity

In terms of spot market prices, the SMM 1# refined nickel price showed a gradual decline throughout May, with an average price of 124,683 yuan, down 1,012 yuan/mt MoM from April. The average premium for 1# Jinchuan nickel in May was 2,200 yuan/mt, a decrease of 300 yuan/mt MoM from 2,500 yuan/mt in April. In terms of trading, restocking activity after the Labour Day holiday was short-lived, with some downstream players restocking at lower prices, but the momentum was insufficient. Spot trading in May was mainly driven by immediate demand, with low enthusiasm for stockpiling among enterprises.

2. Weak Supply and Demand: Global Nickel Market Surplus Persists

According to SMM data, refined nickel production in May 2025 was approximately 35,000 mt, down 2.6% MoM but up 37.8% YoY. In June, affected by the decline in nickel prices, production schedules at some smelters are expected to decline, leading to a continued MoM decrease in overall production.

Demand also showed structural weakness:

Stainless Steel Sector: Confidence in the stainless steel industry remains low, with steel mill profits under pressure and production schedules declining MoM. The off-season effect is evident, with steel mill inventories accumulating and purchase willingness suppressed. Nickel demand is mainly driven by immediate needs.

New Energy Sector: From January to April, China's cumulative installed capacity of power batteries reached 184.3 GWh, up 52.8% YoY. Among them, the cumulative installed capacity of ternary batteries was 34.3 GWh, accounting for 18.6% of the total installed capacity, down 15.9% YoY. The dominant position of LFP has strengthened, with an increased market share, further squeezing the application space for nickel in power batteries.

Alloy and Special Steel Sector: Current demand for alloy and special steel remains stable, with SMM estimating alloy demand for refined nickel at approximately 13,000 mt in May. As this sector accounts for less than 10% of downstream nickel demand, it is not enough to reverse the surplus.

3. High Inventory Pressure: Global Visible Inventory Continues to Accumulate

Inventories at the London Metal Exchange (LME) continue to climb. As of May 29, LME nickel inventories reached 200,142 mt, a decrease of approximately 1,788 mt from the beginning of the month. Domestic inventories showed a mixed trend: SMM's six-location social inventory experienced a slight destocking, decreasing by 2,535 mt from the beginning of the month to 41,553 mt at month-end. Bonded zone inventories continued to decline, decreasing by 900 mt in May to 5,000 mt, with the import window remaining closed.

4. Macro Disruptions and Policy Uncertainties Dominate the Market

Early in May, China and the US reached an agreement to "remove tariffs on 91% of goods," marking a breakthrough in trade easing between the two countries. This has alleviated cost pressures on export-oriented manufacturing industries and also eased export pressures on nickel-downstream stainless steel and battery materials, improving market expectations for metal demand. Meanwhile, China's central bank, the National Financial Regulatory Administration, and the China Securities Regulatory Commission jointly announced a package of financial policies to stabilize the market and expectations, enhancing expectations for liquidity easing and warming market sentiment for industrial products.

However, by late May, the market's optimism over the reduction of China-US tariffs had been fully absorbed, lacking new driving forces. On May 20, the central bank cut the LPR rate by 10 basis points, but corporate and household credit demand remained sluggish, with weak willingness for real consumption and investment. The effect of liquidity release on boosting metal demand was not significant, and nickel prices struggled to rebound.

At the end of May, market rumors emerged that Indonesia's quota had increased to 320 million wmt, prompting short-sellers to enter the market. On the same day, the open interest of the most-traded SHFE nickel contract surged to 107,000 lots, and nickel prices fell by 2% in a single day. However, after verification by SMM, the news was found to be false. Indonesian authorities stated that there had been no large-scale approval of supplementary quotas in the past two weeks. Subsequently, nickel prices rebounded, with LME nickel prices returning to the $15,300/mt level and the most-traded SHFE nickel contract rebounding to 121,000 yuan/mt.

Overall, the sharp fluctuations in nickel prices in May were mainly due to macroeconomic disturbances. After excluding abnormal disturbances in candlesticks, SHFE nickel futures prices mainly showed a slow decline under the dual pressures of "weak fundamentals" and "high inventory". After the Dragon Boat Festival, whether the stockpiling demand of downstream enterprises can be released will test the strength of price support. Currently, nickel prices are struggling at the edge of the cost line, and industry restructuring may accelerate. Looking ahead, the supply surplus pattern is difficult to change, with a lack of bright spots in demand and weak macroeconomic boosts. The rising cost of Indonesian nickel ore provides some support for nickel prices, and it is expected that nickel prices will remain in a range of weak oscillations.

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn